I went on a search to find cheap massage insurance.

I found two options. One for $94 and the other for $96.

But deciding on which massage insurance to buy is not as straightforward as finding the cheapest.

Many organizations bundle massage insurance in with membership.

Membership comes with bonuses, like “free” massage CEs, but surprise, surprise, bundled packages typically cost more.

Hmm…paying a little more to get “free” CE courses sounds good…but wait, renewal is every 2 years (if you’re in PA)…should I pay a little more to get “free” CEs every year?…am I really saving money?…and what if I hate the CE courses…hey, this one gives me a free website…but wait, I don’t own the domain name…

Ugh!

Take a deep breath in. We can get through this – and it’s important to get through this. Why?

Why I Have Massage Insurance

My number one reason to have massage insurance is to protect me against client injuries. If I make a mistake or if I am accused of making a mistake, I want some liability protection. For that protection, you’ll pay anywhere from 74 cents/day for a policy with professional amenities (like access to free rental agreement forms) to 26 cents/day for a policy with no bells and whistles.

In addition to the massage insurance policies being affordable, I have confidence that the massage insurance providers will be there for me if I need it. I say that for a reason.

The Good Old Days

If you haven’t been doing massage as long as I have, you won’t remember the good old days when you just bought cheap massage insurance and that was it.

No “free” websites that never get noticed.

No newsletters that you never read.

No upselling you scheduling software and massage business services.

No massage insurance the next year because the company you bought from vanished into thin air! (Yep, that happened to me.)

Okay, so it wasn’t all that great.

The reality is, we’ve got a lot of choices now.

We just need to wade through them–and that’s what I’m going to help you do.

Before we get started please note that some of the links below are affiliate links. That means I get a paid a fee if you purchase through an affiliate link. But you don’t pay more for going through my links.

Affiliate fees help keep this blog going, and thank you if do choose to support my work.

My goal with this article is simply to give you the spreadsheets so that you can compare policies. You make the decision regarding who you want to go with.

Lastly, if you have a massage insurance liability question for any company mentioned in this article, send it to me. I will make sure that you get an answer.

Sound good?

Alright, let’s get started.

Here’s What I Did to Find Cheap Massage Insurance

To make things easier, I divided up the many massage insurance options into two categories: Just Insurance and Insurance with Extras.

Here’s what a Google search turned up for the Just Insurance options.

Just Massage Insurance

a. $94/year: Insure LMT

b. $96/year: Insure Bodywork (BBI)

c. $109/year: American Massage Council

Here are the Insurance with Extras options.

Massage Insurance with Extras

a. $175/year: Hands On Trade

b. $169/year: Massage Magazine Insurance Plus

c. $179/year: NACAMS

d. $199/year (and $229/year): ABMP

e. $204.99/year: NAMASTA [$99.99 (associate membership) + $105 (insurance)]

f. $235/year: AMTA

g. $269/year: Alternative Balance

In this category there are 7 options.

Now let’s compare the options in Just Massage Insurance.

I Just Want Freakin’ Massage Insurance

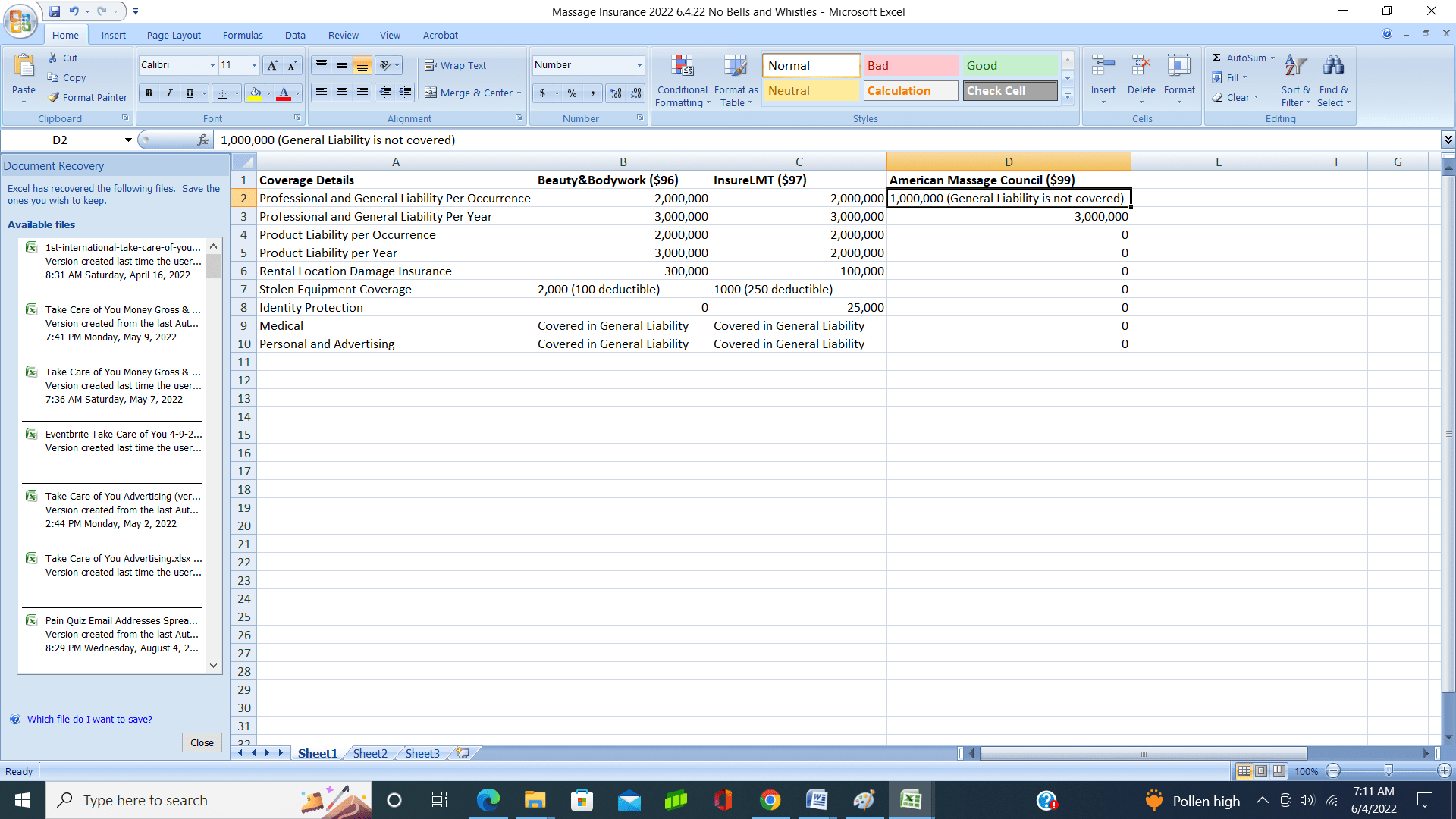

Here’s what the 3 options for Just Massage Insurance look like on a spreadsheet:

Immediately you see that the American Massage Council’s policy is lacking in 8 out of 9 categories when compared to Insure Bodywork (BBI) and Insure LMT.

In 5 out of 9 categories, both Insure Bodywork (BBI)and Insure LMT provide the same coverage amount. Of the 4 remaining categories, Insure Bodywork (BBI) wins: 3 (win) -1 (loss).

So, Insure Bodywork (BBI) is $2 more than Insure LMT, but is better than Insure LMT in 3 categories.

Claims Versus Occurrence Insurance Policies

Both InsureBodywork (BBI) and Insure LMT are occurrence policies. BBI was a claims policy but switched to occurrence near the end of 2024.

That’s a good thing. Here’s why:

Allen Financial Insurance Group explains the difference between a claims policy and an occurrence policy:

A claims policy covers the insured for an incident that occurred during the policy period and was reported as a claim while the policy remained in force.”

An occurrence policy “provides coverage for ‘alleged incidents’ (injuries) that happened during the policy year regardless of when the claim is reported to the carrier. It provides a separate coverage limit for each year the policy is in force. It doesn’t matter if the policy is active when the claim is reported. It only matters that the policy was active when the alleged incident occurred.”

Huh?

I’m with ya. Let’s put it in massage language.

A Claim Happens

You have an occurrence massage liability policy.

Kyle, a client, trips over your massage stool and breaks his wrist when the policy is in effect (while you have the occurrence insurance).

The next year you buy a different massage liability policy and that next year Kyle makes a claim.

No problem because you’re covered under the occurrence policy that you had the year before even though you no longer have that policy.

Now, say you had a claims-made policy when Kyle tripped and broke his wrist. But the next year (the year Kyle makes a claim) you had a different insurance policy.

Guess what?

You’re not covered because the claim was made when your claims-made policy was not in effect.

In the Kyle scenario in order to be covered with a claims-made policy you would have had to renew your claims-made policy the year Kyle reported a claim.

Important stuff to know, but not the end of the world, right?

So, like I said before, the good news is that both Insure Bodywork (BBI) and InsureLMT are occurrence policies.

So, if you want to save a couple of bucks, go with InsureLMT.

If you want higher payout limits in a couple of categories, go with InsureBodywork (BBI).

Massage Insurance with the Bells and Whistles

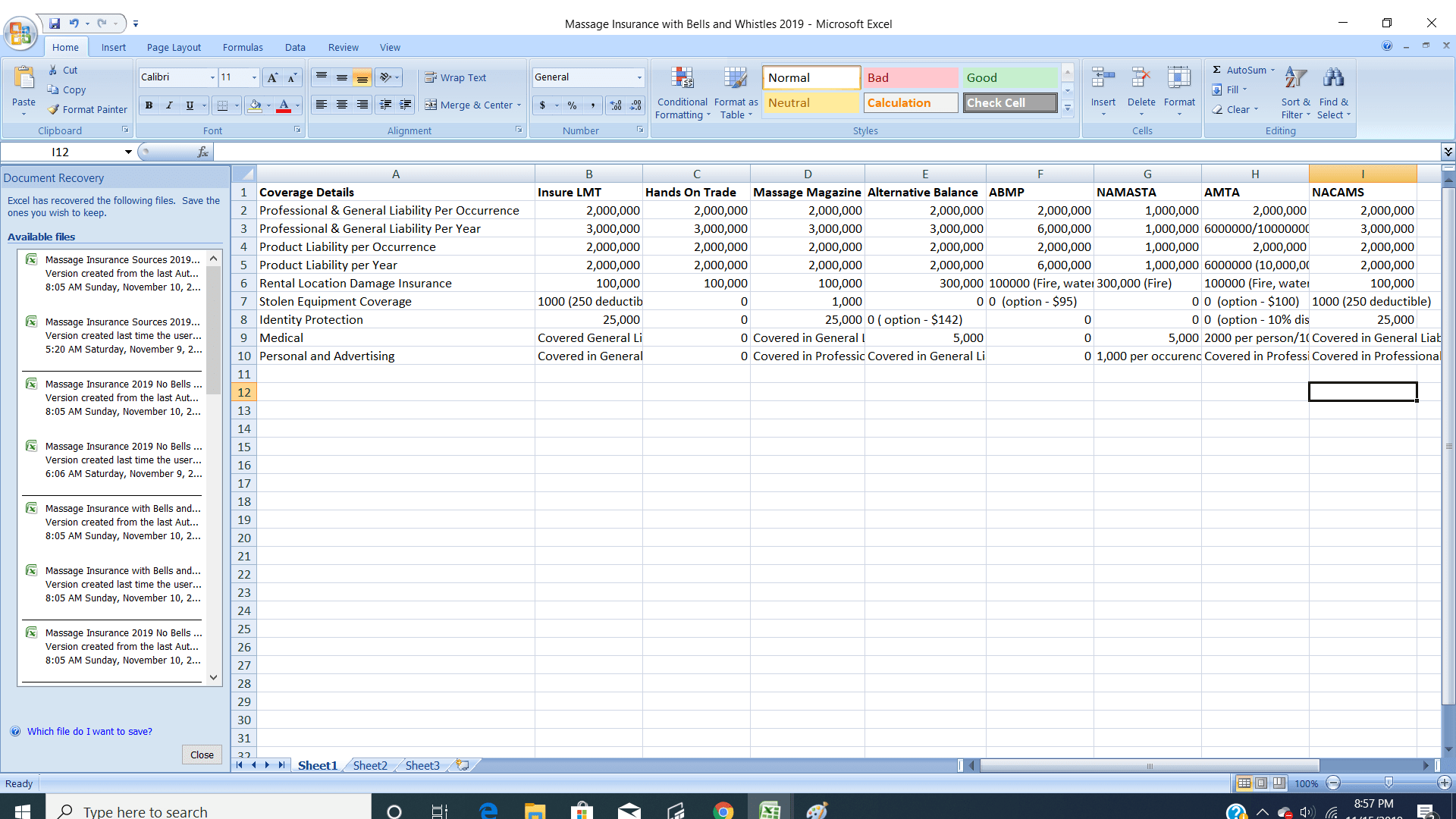

Take a look at the spreadsheet:

A quick glance reveals that in categories 1 – 5 all options are fairly comparable except for NAMASTA. Their numbers are the lowest.

Also, worth noting is that the ABMP and AMTA have the best numbers in categories 1 – 5.

Let’s look at categories 6 – 9. HandsOnTrade scores the worst. And ABMP, AMTA and NAMASTA have goose eggs in two out four categories.

NAMASTA is looking a little rough here. We’ll come back to that a little later.

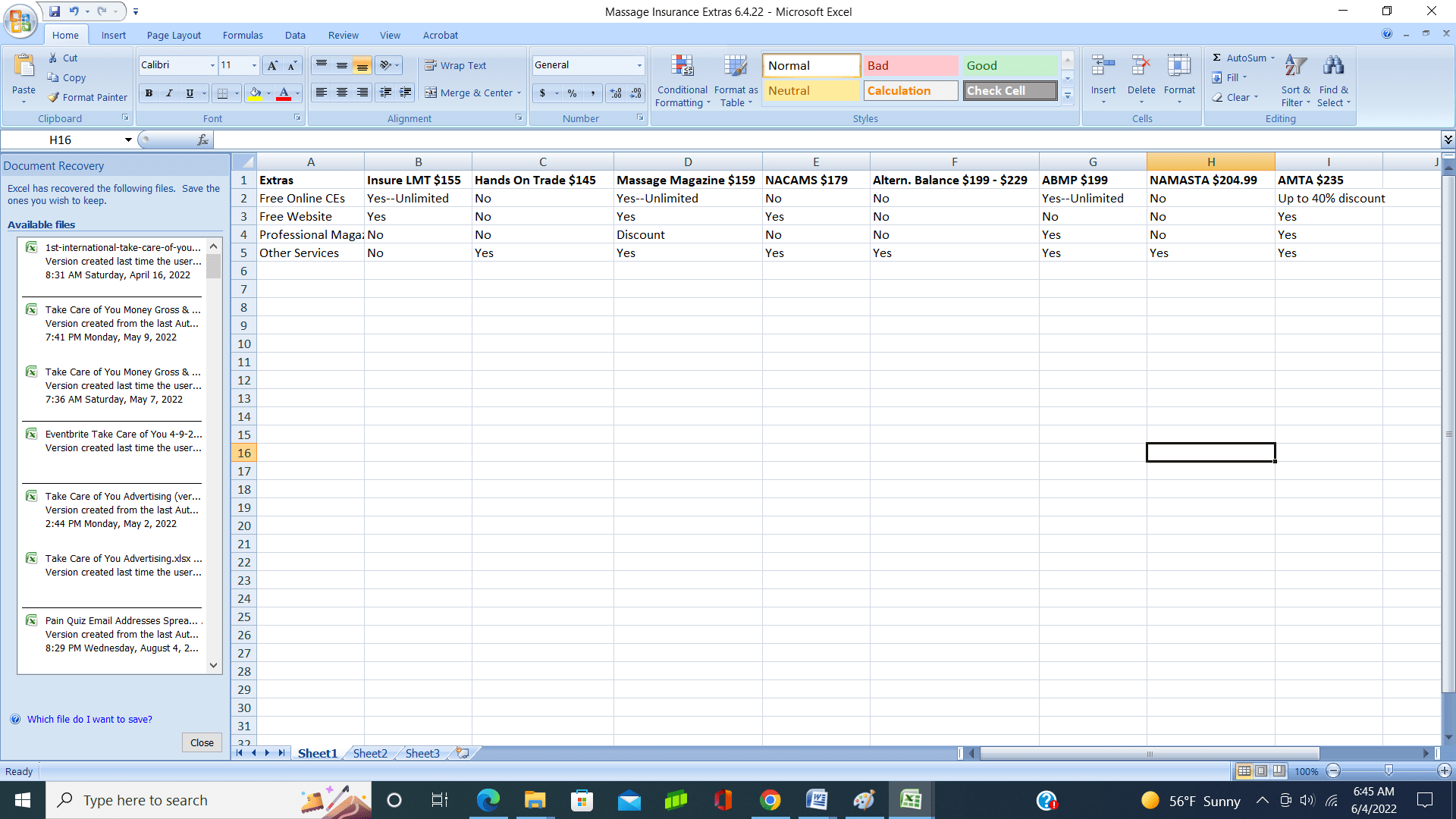

But what about added value? Here’s a spreadsheet of the extras you get with each option.

At this point, if I were leaning towards buying insurance through a professional organization, I’d look at the column that is labeled “Extras” and decide which extras are important to me.

Once you decide what’s important to you, it will be easier to select a professional organization that meets your needs.

Free Websites Don’t Work

Okay, I have to say something here.

If you’re jacked about the free website you’re going to get with your insurance, don’t be.

It will be as generic as vanilla ice cream and your URL will be unprofessional and make the client wonder if you can afford sheets.

Build a massage therapy website yourself (as cheap as $60/year to start).

Okay, back to the business of picking insurance.

Massage Insurance Bundle Deals

You might be wondering if a bundle deal through a professional organization could save you money via the bonuses and perks.

Good question.

Here Massage Magazine Insurance Plus ($169) stands out because they offer unlimited online CEs and have solid insurance. Massage Magazine Insurance Plus also throws in $500+ in industry discounts..

But before you whip out your Visa, here’s something to think about…is buying an insurance option with unlimited CEs cheaper than buying BBI at $96 of InsureLMT policy at $97 and getting your CEs elsewhere?

Well, today I found 24 online CEs for $55. So, the answer would be you if you want the absolute, cheapest massage insurance and an online CE combo then buying an insurance policy with no bells and whistles and finding a cheap online CE provider can save you a little bit of money.

But if you want cheap, no hassles and unlimited CEs always at your disposal, go with Massage Magazine.

It’s Not Always About the Money

But buying massage insurance through a professional organization isn’t always about money, right?

Sometimes it’s about category 4–“Other”. In other words, it’s about having the support of a professional organization.

For a deeper dive into “Other”, here are the links to the additional perks with each option. I’ll see you in the paragraph after the links. (Oh, warning: when you see the word “access”, that usually means you have access to something that you’ll have to pay for.)

How’d it go? Did one organization resonate with you? If so, maybe that’s the one to buy from. But before you do, let’s do a quick review.

My Massage Insurance Cautions

These massage insurance options fell significantly short of their competitors.

In the Just Insurance category, the American Massage Council insurance coverage was the weakest

And NAMASTA fell behind the rest of the pack in the Insurance with Extras category.

But if you liked the extras NAMASTA offers, you could become a member (and get the extras) without buying the massage insurance from them.

And in Conclusion…

Does it seem like it’s getting complicated again?

Let’s un-complicate it.

Do you want cheap massage insurance?

If so, go with the least expensive Insure LMT ($94) or Insure Bodywork (BBI) ($96) with higher coverage in damage to premises rented to you and medical expense coverage.

Do you want cheap massage insurance and “free” CEs?

Then go with Massage Magazine Insurance Plus ($169 with unlimited CEs and the massage industry discounts).

Do you want the support of a professional organization?

Decide which organization has the perks that are best for you. And if at the end of a year, it turns out to be a bad fit, you can always switch to another option.

It’s your hard-earned money.

Spend it where it makes the most sense for your needs.

Massage Insurance Q & A

What type of insurance does a self-employed massage professional need?

Another way of asking this question is: as a self-employed, sole proprietor, massage therapist, do I need additional insurance beyond massage insurance (professional liability insurance) such as a general liability policy (protects against third-party injuries or property damage occurring on your premises)? The good news is that most massage insurance policies have some kind of general liability protection included in their policies. Here are three examples:

1. American Massage Therapy Association (AMTA):

- Professional Liability Insurance: AMTA provides professional liability insurance with coverage limits of up to $2 million per occurrence and a $6 million annual aggregate. This coverage includes general liability, which protects against third-party injuries or property damage occurring on your premises.

2. Associated Bodywork & Massage Professionals (ABMP):

- Professional Liability Insurance: ABMP offers professional liability insurance with coverage limits of up to $2 million per occurrence and a $9 million annual aggregate. This policy includes general liability coverage.

3. Massage Magazine Insurance Plus (MMIP):

- Professional Liability Insurance: MMIP provides professional liability insurance with coverage limits of up to $2 million per occurrence and a $3 million annual aggregate. This coverage includes general liability.

What you have to decide: While these policies offer substantial coverage, it’s important to assess whether they meet your specific needs. For instance, if you own your practice space, you might need additional commercial property insurance to protect your equipment and workspace from damage or theft. Additionally, if you offer specialized services or have unique risks, you may require higher coverage limits.

Best Practices:

- Review Your Policy: Carefully read the terms and conditions of your insurance policy to understand the coverage limits and exclusions.

- Assess Your Risks: Evaluate the specific risks associated with your practice, such as the value of your equipment, the nature of your services, and the location of your practice.

- If you need more help, consult an Insurance Professional: Consider speaking with an insurance agent who specializes in massage therapy to ensure you have adequate coverage tailored to your needs.

Do I have to have massage insurance?

If you work for someone, they probably require massage insurance – and some states do, too. In addition, some cities and counties may have their own rules. You’ll have to do your research.

Can I get massage insurance if there is no licensing in my state or my modality is not recognized under massage state licensing?

The answer is yes. For a deeper dive, go here to see the specifics and to find out which massage insurance providers don’t require proof of training.

I don’t have the money upfront – are their policies I can buy month to month?

Yes. Insure Bodywork (BBI) offers $9.99/month.

Insurance Terms

Here’s a list of insurance terms and definitions to use as a reference. All are taken from the HandsOnTrade website, except for one definition that is noted. I made one grammatical edit to Hands On Trade definitions.

Claims Made Policy : Claims-made policies provide coverage only for claims that are made while the policy is active. If your claims-made policy expires, and someone files a claim against you later, you would have no coverage, even though you were insured at the time of the incident. (Osborne, Karrie, What Are Your Risks?, Massage & Bodywork Journal, January/February 2014.)

Occurrence Based Policy: Insurance that pays claims arising out of incidents that occur during the policy term, even if they are filed years later or if the policy is no longer in effect.

Malpractice: Professional misconduct or lack of ordinary skill in the performance of a professional act which renders the practitioner liable for damages.

Professional Liability Insurance: The obligation that a professional practitioner has to provide care or service that meets the standard of practice for his/her profession.

General Liability Insurance: A form of insurance designed to protect practitioners from liability exposures arising out of accidents resulting from the premises.

Product Liability Insurance: Insurance on a professional practitioner from suits arising out of damage caused by a product used on a client.

Damage to Premises: Property Damage to any one premises while rented by the Insured or in the case of damage by fire, while rented by the Insured or temporarily occupied by the Insured with permission of the owner of premises.

Per Occurrence limit: This is the limit for all damages, whether property damage or bodily injury resulting from one occurrence.

Aggregate limit: This is the maximum limit for all claims against you during the policy period. Each claim paid reduces the remaining coverage for the period until the aggregate amount is paid.

Free Resources

If you’re trying to build a massage business without spending a lot of money, this free program will help you out: Jumpstart.

Check out more ways I save money on my resources page.

Sign up to be in my email group to get my latest information.

Last, if you find this information helpful and want to continue to hear a perspective outside the usual industry voices, please share this cheap massage insurance guide. It’s the only way this kind of independent insight gets out there—and it helps more therapists like us stay informed.

About Mark Liskey:

Mark is not a bot. He is a business owner, neuromuscular massage therapist of 30+ years, teacher, writer and blogger. In this blog, he shares best practices for inexpensively growing a business. You can also find Mark’s articles here: Massage Magazine and Massage & Bodywork Journal. Mark loves working in his massage businesses – PressurePerfect Massage and Pain-Free Massage Therapist.

Comments on this entry are closed.

Thank you so much! Last-minute shopping for insurance (have had my license for a while but just decided to pick up gigs now that I’ve quit my desk job) and this is very helpful!

Hey Rae, glad you found it helpful! Let me know if there is anything else I can help you with!

Hello Mark .. Ty for this very detail oriented and informative website .. I was hoping you could clarify something on the 1st spreadsheet .. “No Bells and Whistles” .. Row #9 has a heading that says MEDICAL and it shows that BBI Company has zero .. I called BBI and asked about their medical coverage .. they said if a patient gets injured while at your place or in your care we will cover their medical expenses up to the 2 million per occurrence .. Mark I’m confused, can you please explain your meaning of the word MEDICAL in Row #9 ?

Hey T-man, thanks for the question. I appreciate your diligence. The column that says MEDICAL (Row #9) refers to Medical Expenses. I’m defining medical expenses as “Coverage that reimburses others, without regard to the insured’s liability, for medical or funeral expenses incurred by such persons as a result of bodily injury or death sustained by accident under the conditions specified in the policy. This does not apply to the named insured or their employees.” (I’m using the definition given on the Alternative Balance Website, https://alternativebalance.net/coverage_cost).) So, MEDICAL in row #9 does not stand for a medical expenses maximum amount that will be covered if someone gets injured at your place. Sorry for the confusion. I will be updating this article soon to reflect any changes with insurance providers and I will provide more clarification with the terms then. Thanks!

I am happy to hear the part about updating your website soon with more clarification .. because the explanation you just wrote is still very confusing .. what I understand is BBI offers zero coverage for something medical .. but I still unsure sure what that something is .. is it funeral expenses ?

Sorry to leave you hanging, T-man. As it was explained to me, the key thing is who’s at fault. When you’re at fault, medical expenses, etc. are usually covered in the general liablity coverage. If you look at the spreadsheets, all companies cover this including BBI (at the 2 million per occurence that you had mentioned). When you’re not at fault (e.g., someone slips in the parking lot and comes after your business because it happened in the parking lot but the accident is not directly related to you) that is covered under the category of medical expenses. At the time of the blog post I had called the insurance providers and/or professional organizations that sold the insurance to see if medical expenses (without regard to fault) were covered in their policies if not stated on their websites. Not sure if there was a miscommunication with BBI or BBI added medical expenses more recently to their policy, but it turns out that BBI does cover $5,000 per incident. So, I will be updating the spreadsheets and article soon. Great question and comments. Thank you. It all helps me with clarifying and simplifying when I do the update.

Ahhh, just what I was looking for. Added perk that you broke down the CEs for PA!! Much love, thanks!!!

Hey, Jen! Glad the article was helpful. Let me know if there’s something else you need more info about. Take care!

Thanks for the info and breaking it down in an approachable way. It can be a little overwhelming, but this really eased my mind! Best of luck with your business!

Hey Eric, I’m glad the article helped you out! Good luck, and I’ll be here if you need more info and/or help with massage stuff:-)

Thank you for this! I relocated and just received my Georgia license and was trying to figure out which policy to go with…you helped me make that decision, so thanks! 🙂

Hey, I’m glad that I could help you out! Good luck and let me know if there is another topic that you’d like more information about.

Any recommendations for malpractice, liability insurance for bio-magnetic pair therapy practitioners? Also, I’m looking for advice re. crafting a hold harmless agreement, for clients to sign.

Hey, Lee! I’m not sure about liability insurance for biomagnetic therapy, but I’ll look into it and get back to you.

Regarding a hold harmless agreement, the AMTA provides a sample here: https://www.amtamassage.org/career_guidance/detail/102?typeId=3

And here’s an example from the ABMP: https://www.abmp.com/members/pdfs/client_information.pdf

Hopefully, they will help as you re-craft your hold harmless agreement.

I’ll let you know what I find about liability insurance for biomagnetic therapy.

Thanks for the useful breakdown! Readers should note: BBI does NOT cover cupping–definitely not wet (heat/blood-drawing), but not even dry; they charge extra for it. So, the $96 suddenly becomes over $130. ILMT is a lot more comprehensive from that perspective.

Thanks for the information about the difference between BBI and ILMT insurance coverage for cupping! That’s really helpful to know and important to consider even if cupping is only a minor treatment therapy in one’s massage regimen.